Revolut, a popular digital banking platform with over 45 million customers worldwide, is increasingly facing scrutiny due to a growing number of fraud cases. A series of BBC reports have highlighted instances where Revolut customers lost significant sums of money to fraudsters, raising concerns about the platform’s security measures and customer service response. While Revolut promises robust controls and advanced technology to combat fraud, the experiences of these customers suggest otherwise, prompting an urgent need for greater accountability and improved protection.

The Rise of Fraud Cases Involving Revolut

As Revolut has grown into one of the most successful fintech platforms, offering a range of services such as currency exchange, cryptocurrency investments, and global money transfers, it has also become a target for fraudsters. Despite the platform’s claims of having strong anti-fraud mechanisms, several high-profile cases have raised questions about the company’s ability to safeguard its users’ money.

One such case, reported by the BBC, involved Jack, a business owner who lost £165,000 in just one hour. Fraudsters gained access to his Revolut business account by tricking him into revealing security details over the phone. Jack was led to believe he was speaking to Revolut’s security team after being told his account was compromised. In reality, the scammers were setting up fraudulent payees, draining his account through multiple small transactions. Jack immediately contacted Revolut, but it took 23 minutes for the company to respond via their app-based chat service, during which an additional £67,000 was stolen. Revolut has so far refused to refund the money, stating that it is investigating the case.

Another victim, Dr. Ravi Kumar, an NHS consultant, lost £39,000 after scammers convinced him to transfer his savings into his Revolut account, claiming it was a secure place to protect his funds. They later accessed the account and spent the money on luxury items. Dr. Kumar, like many others, was denied a refund because Revolut claimed he had authorized the transactions. He has since hired legal help to pursue his case with the Financial Ombudsman Service (FOS), highlighting the financial and emotional toll such incidents take on victims.

Why Revolut Is Vulnerable

One of the key vulnerabilities of Revolut, as illustrated by these cases, is its reliance on digital-only infrastructure. Unlike traditional banks, which have physical branches and dedicated phone support lines, Revolut manages everything through its app. This has become a significant pain point for customers who need urgent assistance during fraud incidents. The lack of an emergency helpline meant that both Jack and Dr. Kumar had to rely on slow in-app messaging services, giving scammers more time to deplete their accounts.

Additionally, fraudsters have found ways to exploit one of the most common security mechanisms in online banking: the one-time passcode (OTP). OTPs are supposed to provide an extra layer of protection during transactions, but scammers have developed tactics to trick users into sharing these codes, allowing them to bypass Revolut’s defenses. In Jack’s case, the scammers used detailed knowledge of his recent transactions to convincingly pose as legitimate Revolut employees.

Fraud prevention experts have criticized Revolut’s rapid expansion and the wide array of financial services it offers as potential sources of weakness. The company’s all-in-one financial app allows users to hold multiple currencies, trade stocks, buy cryptocurrencies, and manage their finances from a single platform. However, this convenience also creates a high-risk environment where, if compromised, fraudsters can gain access to significant financial assets in one place.

The Extent of the Problem

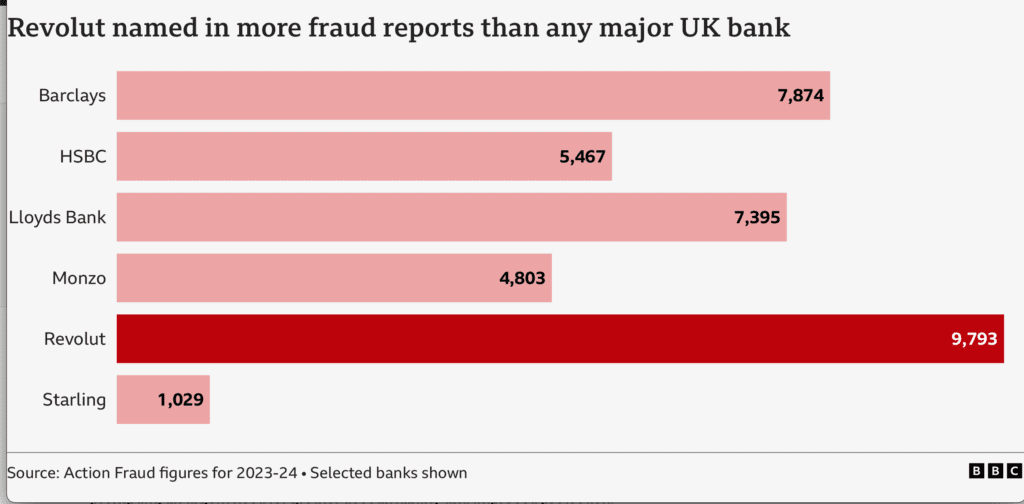

Revolut’s fraud problem is not isolated to just a few cases. According to BBC’s investigations, Revolut was mentioned in almost 10,000 fraud reports filed with Action Fraud, the UK’s national reporting center for fraud and cybercrime, in the last financial year. This figure surpasses those of major high-street banks like Barclays and is double that of Monzo, another fintech competitor of similar size.

Despite this troubling statistic, Revolut has continued to grow at a rapid pace, reporting record revenues of £1.8 billion in 2023. The company insists that it is investing heavily in its anti-fraud measures and that financial crime prevention now makes up over a third of its workforce. Yet, former employees and fraud specialists interviewed by BBC Panorama point to a high-pressure corporate culture focused on rapid growth and new product launches, with fraud prevention often playing second fiddle to expansion.

This has left many customers feeling neglected and unprotected. One of the most severe cases involved Lynne Elms, who lost £160,000 from her employer’s business account after scammers convinced her to install remote desktop software. They then took control of her computer and transferred the money to fraudulent accounts within minutes. Revolut’s slow response meant that the scammers were able to complete multiple transactions before the account was frozen.

New Regulations and Challenges for Revolut

The UK government has recently introduced new mandatory rules to address the rise in authorized push payment (APP) fraud. These rules, which took effect in October 2024, require banks and e-money institutions like Revolut to refund victims of APP fraud up to £85,000 within five days. This shift from a voluntary code to mandatory regulations places additional pressure on Revolut to handle fraud cases more effectively and could result in significant financial liabilities for the company.

In the first half of 2024 alone, there were 97,344 reported cases of APP fraud, resulting in £214 million in losses. With the new rules in place, Revolut may find itself reimbursing more victims, which could pose a challenge given its higher-than-average number of fraud reports.

While Revolut has introduced some new measures, such as AI-powered fraud detection tools and biometric identification features, these have yet to fully restore confidence among users. The company’s reputation has been tarnished by the high-profile fraud cases reported in the media, and its customer service—particularly the lack of immediate human support—remains a significant issue.

Conclusion

Revolut’s position as one of the leading digital banking platforms has made it a prime target for increasingly sophisticated fraud schemes. The experiences of customers like Jack, Dr. Kumar, and Lynne Elms illustrate the potential weaknesses in Revolut’s security infrastructure and customer service response. While the company has invested in anti-fraud measures and continues to expand its offerings, the growing number of fraud cases linked to the platform raises questions about whether these efforts are sufficient.

As new regulations take effect, requiring quicker and more comprehensive reimbursements for fraud victims, Revolut will need to significantly improve its fraud detection and prevention capabilities. Failure to do so could not only result in financial losses but also in long-term reputational damage, undermining the trust that millions of customers have placed in the platform. In the ever-evolving world of digital banking, security must be as much of a priority as growth and innovation.