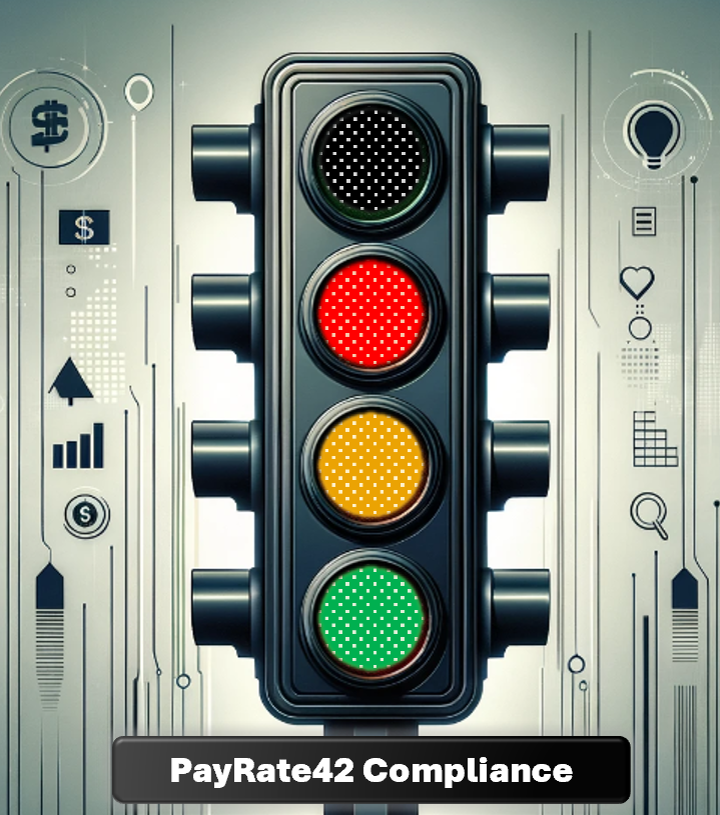

1. Compliance Color Coding

PayRate42 (PR42) has established a unique review and rating system, aptly termed CyberFinance, to assess financial service providers in the digital realm. The evaluation of financial services providers involves an assessment of the risk that their customers are taking. Adherence to compliance rules is one of the most important factors in minimizing risk.

Our system utilizes a traffic light color coding to offer clear guidance for potential clients and partners:

- GREEN: Represents a provider compliant with laws and norms;

- ORANGE: Indicates some compliance concerns;

- RED: Signifies substantial compliance concerns;

- BLACK: Black is used for companies associated with malicious businesses.

Our evaluation encompasses compliance, legal security, and transparency based on website information, regulatory warnings, customer reviews, and financial data.

2. Compliance Criteria Guideline

2.1 Green Signal

In our Compliance Color Coding scheme, we include a financial services provider in the CyberFinance space in our Green Signal compliance list based on the following findings:

- Authorization: The financial services provider is authorized to conduct its business in the targeted regulatory regimes;

- Transparency: The provider’s website, terms, and service agreements provide all necessary information (founder(s), legal entities, regulatory license/permissions, jurisdiction, social media);

- Client Feedback: Not too many negative reviews, ratings, or comments on Trustpilot, Google, and other review & rating sites.

- Other: financial information

Find our Green List here.

2.2 Orange Signal

We include a financial services provider in our Orange Signal compliance list based on the following findings:

- Authorization: We could not establish that the provider has regulatory authorization for all jurisdictions it offers its financial services.

- Transparency: The website, terms, and services agreements do not provide the required information, and/or the information is difficult to find (founder, legal entity, license, jurisdiction & social media);

- Client Feedback: Predominantly bad reviews and ratings on Trustpilot, Google, and other platforms.

- Other: financial information

Find our Orange List here.

2.3 Red Signal

We include a financial services provider in our Red Signal compliance list based on the following findings:

- Authorization: We found that the payment processor is not authorized to run its business;

- Transparency: The website provides false or misleading information;

- Founders with a questionable track record (not fit and proper);

- Client Feedback: Poor customer ratings and reviews and/or regulatory warnings against clients of the financial services provider, i.e., facilitates illegal business intentionally or by neglecting KYC/AML obligations.

- Other: financial information

Find our Red List here.

2.4 Black Signal

We include a financial services provider in our Black Signal compliance list on the basis of the following findings:

- Authorization: No authorization, regulatory warnings against the financial services provider and/or its client; involved in money laundering activities,

- Transparency: no information or misleading/false information about the operators is given on the website;

- Client Feedback: reports of defrauding merchants and freezing client funds without proper explanation!

Find our Black List here.

3. Our Compliance Definition

“Compliance” in the financial sector refers to the practice of financial institutions adhering to laws, regulations, guidelines, and specifications relevant to their business operations. This includes a broad range of activities, such as:

- Following Regulatory Laws and Rules: Financial institutions must comply with the laws and regulations set by governmental bodies and financial regulators. This includes, but is not limited to, banking laws, securities regulations, and anti-money laundering (AML) laws.

- Internal Policies and Procedures: Compliance also involves adhering to internal policies and procedures designed to ensure that the institution operates within legal and ethical boundaries.

- Risk Management: Identifying, assessing, and mitigating risks related to legal or regulatory non-compliance is a critical part of compliance. This includes risks related to financial crimes, data security, and operational integrity.

- Reporting and Transparency: Financial institutions are often required to maintain transparent operations through regular reporting. This includes financial reporting, disclosure of potential conflicts of interest, and reporting suspicious activities as part of anti-money laundering efforts.

- Customer Protection: Compliance ensures that financial institutions deal fairly with their customers, providing accurate information about products and services and safeguarding customer data.

- Regular Audits and Assessments: Regular internal and external audits are conducted to ensure that compliance measures are effective and that the institution adheres to relevant laws and regulations.

- Training and Awareness: Ongoing training and awareness programs for employees are essential to maintain a culture of compliance and to keep staff updated on the latest regulatory developments.

In summary, compliance in the financial sector is about ensuring that financial institutions operate legally, ethically, and responsibly, minimizing risks to the institution and its customers, and promoting trust and stability in the financial system.